Your step by step guide to becoming a first home buyer.

Buying your first home is exciting, but can be daunting and confusing. Don't worry! We've cut through the noise to give you a clear, simple breakdown of the key steps, and government schemes to help you get onto the property ladder sooner.

THE LADDER STRATEGY:

Become a first home buyer by leveraging multiple government schemes - Entry is easier than ever, you can buy now with just 5% a deposit needed.

Know exactly you can afford - no guesswork, find your real borrowing capacity and get pre-approved.

Make sure you’re prepared to act - get your approvals, build your deposit and do your research so you can act with confidence

Your 6 step plan to buying your first home

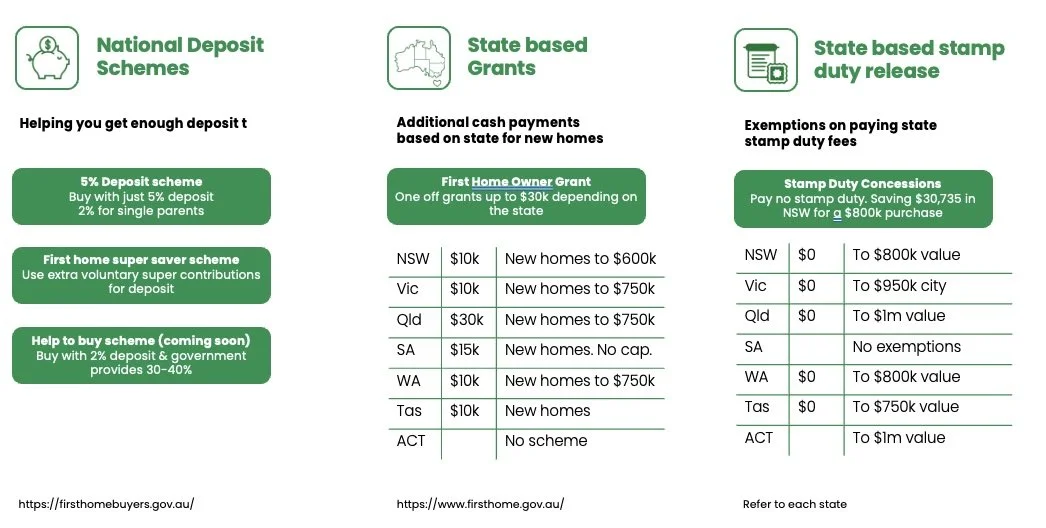

STEP 1: Understand your eligibility for various first home buyer schemes

The headline here is the government’s new 5% deposit scheme, but actually there are actually many different schemes available, and many variances by state. The table below outlines the main schemes.

The first step is to understand what you’re eligible for. There are some income and property price caps so speak to us, or start researching. It can be confusing, so we’re happy to help guide you through the schemes, and check your eligibility.

The good news is that you can stack some of the different schemes on top of each other. This provides a great incentive to get into the market.

Note: Specific eligibility rules apply and there are many variations e.g. higher caps for regional areas

STEP 2: Know your borrowing power (the real number)

The single most important step after checking eligibility is knowing your true borrowing ceiling. This it’s a critical piece of strategy.

Find out what’s possible: A first home buyer discovery call is an easy way to start the process. In 30 minute we can see what’s possible, and the steps you need to take to become a first home buyer.

Calculate Your Capacity: Your borrowing capacity is the maximum amount a lender will realistically give you. It’s calculated based on your income, expenses, and debts. Knowing this number gives you a non-negotiable budget and stops you wasting time on properties out of your reach. We capture some key information from you so

Secure Pre-Approval: Getting pre-approval confirms your borrowing capacity so you can bid confidently at auctions up to your limit. We prefer unconditional pre-approval which means a human’s reviewed all your situation (not an automated response) so you know exactly what’s possible.

Strategise Your Deposit: Beyond the schemes, you’ll also need a plan to reach you deposit amount. The new 5% deposit scheme means you’ll only need a $25k deposit for a $500k property. So the entry point is getting easier for for first home buyers. However this benefit is balanced out by the fact you’ll have to borrow the other 95%.

How much have you saved? Do you have an efficient savings plan?

Key watch out. Most banks want 5% “genuine'“ savings built over 3 months. Not a windfall. But accumulated over time. So start early and consistently. There is one bank exception, but they may not suit your situation.

STEP 3: Be prepared to take action

Now you’re ready to enter the market. It’s important to do your research on the type of area and property you want to buy,, and what costs of owning a home are.

Mastering Market Selection: To move up the ladder later, your first property needs to be a good investment & right for you.

Buy Smart: Research areas with future infrastructure investment, good transport links, and desirable amenities.

Find your ‘comfortable’: Find an area or property you’re comfortable to live in. You may need to change your location from renting so think about what you’ll be happy with. Don’t forget, it’s not your forever home, so be happy to make a few compromises.

Hold for Growth: Real estate is a long-term asset. Holding onto the property for several years, allows the equity to build, which then becomes your deposit for your second, bigger home.

Property Type: Think about whether you’re buying a new build (to get the FHOG) or an established home or unit? This decision must align with your budget and long-term goals. Some new builds especially apartments carry some risks.

Understand your ongoing costs: Prior to purchase, we’ll provide you with clear information on what your mortgage repayments might be, so you can budget appropriately

Build a buffer: Beyond the mortgage, ensure you have an adequate buffer of savings for ongoing costs like council rates, insurance, and maintenance.

STEP 4: Check you’re ready to be a first home buyer

We all know renting can be a nightmare, and many first home buyers can’t wait to have their own place. Having done the steps above, the next question you should ask yourself is - Are you ready to be a homeowner?

Buying a home comes with responsibility, so make sure you’re committed to buying and holding your property.

STEP 5: Execute the deal

Crunch time. You’ve done all the preparation, now you’ll need to buy your property. Bidding at auctions can be an adrenalin rush. But if you’ve done the groundwork, know your market and budget, this final stage becomes easier.

Prepare to bid: Finalise your budget, bidding strategy. Go in confident up to your limit. Many first home buyers bid on 5+ properties so it’s normal to miss out on your first opportunity. As deflating as it can be, you will get there!

Adjust your strategy: If rates or property prices change look for different regions, or property types.

Do your checks: Prior to making an offer, do a building and property inspection, and have the contracts reviewed.

Place an offer or did at auction: You’ll either bid at auction, or negotiate a price with the vendor.

5-10% deposit: is usually paid on exchange.

Settlement date agreed: Usually 30 to 90 days when you the purchase is finalised.

We also get final bank approval at this stage, as we now know the exact property you’re buying. Most of the loan application work is done as you’ve already submitted everything in the pre approval stage. However we need to submit the property details and signed contract.

Formal loan approval: We submit the signed contract to lender, the lender orders a property valuation, we get ‘formal (unconditional) approval’ and you sign the loan documents

Final transfers of property to you: Your conveyancer coordinates with lender and vendor's solicitor, funds are transferred; title transferred to you as the buyer

Pay final buying costs: Depending on the purchase price, you may need to pay for final expenses like stamp duty, moving costs, conveyancer fees. It’s important to have money saved to cover these.

STEP 6: Move in!

Success! There’s nothing like the excitement of buying and moving into your new home. There’s a world of possibilities ahead - whether deciding on what colour you’ll paint the house, which succulents for the balcony, or finally being allowed to get a dog.

Ready to make the step up?

The first easy step is simple: Have a conversation and know your borrowing capacity. Everything else flows from that number. We will help you calculate your full potential, combine the right schemes, and set you on a path to not just own a home, but to build real wealth.

Call Will on 0414 877 724 or will@ladderfs.com.au and he’s happy to help guide you through the whole process.

Or book a First Home Buyer Discovery call. https://www.ladderfs.com.au/book-now